Choose from a wide range of NEWCV resume templates and customize your NEWCV design with a single click.

Use professional field-tested resume templates that follow the exact Resume rules employers look for.

Create ResumeIf you’re searching for “insurance agent salary,” you’re likely trying to answer a deeper question:

Is this a stable, scalable, and high-income career—or just another commission-heavy grind?

Here’s the truth most articles don’t explain:

Insurance agent income is not linear. It’s heavily influenced by sales ability, product mix, client retention, and—most importantly—residual income structures.

Top agents build income streams that compound over time. Average agents remain stuck chasing new policies every month.

This guide breaks down real earnings, how compensation actually works, and what separates six-figure agents from those barely surviving.

Let’s start with realistic benchmarks based on current market data and hiring insights.

Entry-level agent: $40,000 – $65,000

Mid-level agent: $65,000 – $120,000

Experienced agent: $120,000 – $250,000

Top 10%: $250,000 – $500,000+

But these numbers only tell part of the story.

Unlike traditional jobs:

Income includes commissions + renewals

Earnings compound over time (if structured correctly)

Income stability depends on retention, not just sales

Understanding compensation is the key to understanding salary potential.

Agents earn commissions from selling policies:

Life insurance: 40% – 100% of first-year premium

Health insurance: 5% – 20%

Property & casualty: 10% – 20%

$1,200 annual life insurance premium

80% commission = $960 upfront

Now scale that across volume.

This is where elite agents win.

Agents earn recurring commissions when policies renew:

Typically 2% – 10% annually

Can last for years

When evaluating top candidates, hiring managers prioritize:

Size of renewal book

Policy retention rates

Client lifetime value

Residual income is the difference between:

Top agencies offer:

Quarterly bonuses

Performance tiers

Profit-sharing

Some agents (especially with companies like :contentReference[oaicite:0] or :contentReference[oaicite:1]) receive:

Base salary: $35K – $60K

Lower commissions

This provides stability but limits upside.

Typical earnings:

Reality:

High churn rate

Heavy outbound sales

Low initial renewal income

Typical earnings:

At this stage:

Renewal income starts compounding

Referral networks grow

Sales efficiency improves

Typical earnings:

Top performers:

Have large books of business

Focus on high-value clients

Operate like business owners

Not all insurance niches are equal.

High upfront commissions

Strong residual income

Income range:

Moderate commissions

High policy volume

Income range:

Lower upfront commissions

Strong renewal base

Income range:

Large policies

High client value

Income range:

Commercial insurance agents are often the highest-paid because:

Businesses require complex coverage

Policies are larger and recurring

Relationships are long-term

Low earners:

High earners:

Top agents prioritize:

Long-term relationships

Policy renewals

Upselling opportunities

Low performers depend on:

Purchased leads

Cold calls

High performers build:

Referral systems

Strategic partnerships

Elite agents build:

Thousands of active policies

Predictable recurring income

Gross income is misleading.

Lead generation costs

Licensing and certifications

CRM systems

Marketing and advertising

Office overhead

Real take-home income can be:

Work for a single company (e.g., :contentReference[oaicite:2])

Pros:

Stable income

Training support

Cons:

Limited product range

Lower earning ceiling

Work with multiple carriers

Pros:

Higher commissions

Flexibility

Cons:

No base salary

Must generate own leads

Top earners are almost always independent.

Represents insurance company

Limited product offerings

Represents client

Access to multiple insurers

Agents: $40K – $150K

Brokers: $80K – $300K+

Brokers often earn more due to flexibility and higher-value deals.

Hiring managers don’t care about:

“I made $120K last year.”

They care about:

Book of business size

Annual premium volume

Retention rate

Policy mix (life vs P&C vs commercial)

High income with no renewal base

Heavy reliance on cold leads

No specialization

Weak positioning:

“I sold insurance policies and met sales targets.”

Strong positioning:

Revenue generated

Policy volume

Client retention

Book of business growth

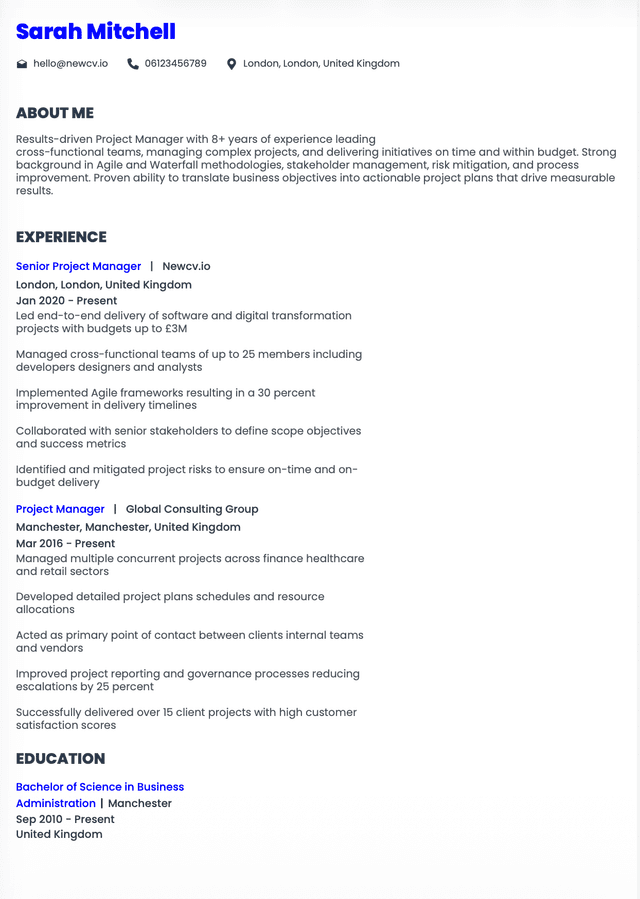

Name: Daniel Rodriguez

Title: Senior Insurance Agent | Commercial & Life Insurance Specialist

Location: Dallas, Texas

PROFESSIONAL SUMMARY

Results-driven insurance agent with 10+ years of experience generating $8M+ annual premium volume across commercial and life insurance portfolios. Proven ability to build high-retention client relationships, scale recurring revenue streams, and consistently exceed sales targets. Expert in structuring complex policies for high-net-worth individuals and businesses.

CORE COMPETENCIES

Commercial Insurance Solutions

Life Insurance Sales

Client Acquisition & Retention

Policy Structuring & Risk Analysis

Revenue Growth & Pipeline Development

Negotiation & Closing

PROFESSIONAL EXPERIENCE

Senior Insurance Agent | Apex Insurance Group | Dallas, TX

2017 – Present

Managed $8M+ annual premium book with 85% client retention rate

Generated $350K+ annual income through commissions and renewals

Closed 120+ new policies annually across commercial and life segments

Built referral network producing 65% of new business

Increased renewal revenue by 40% through upselling and policy optimization

Insurance Agent | Lone Star Insurance | Dallas, TX

2013 – 2017

Built book of business from zero to $3M in annual premium

Specialized in small business and life insurance solutions

Achieved top 10% performance ranking within company

EDUCATION & LICENSES

Licensed Insurance Agent – Texas

Certified Insurance Counselor (CIC)

This creates:

Income instability

No long-term growth

Leads to:

High workload

Low earnings

Without referrals:

Cost of acquisition increases

Growth slows

Top agents operate like:

Entrepreneurs

Revenue managers

Build:

Long-term policy portfolios

Renewal-heavy business

Target:

Businesses

High-value policies

Work with:

Financial advisors

Real estate professionals

Attorneys

Use:

CRM automation

Follow-up sequences

Client lifecycle management

Insurance income fluctuates based on:

Sales cycles

Policy cancellations

Market changes

Top agents stabilize income through:

Large renewal books

Diversified client base

Long-term relationships

Residual income potential

Scalable earnings

Business ownership opportunities

Commission-based income

High competition

Self-driven success

This career rewards:

Consistency

Relationship building

Long-term thinking

It punishes:

Short-term sales mentality

Lack of discipline

Poor client retention

Use ATS-optimised Resume and resume templates that pass applicant tracking systems. Our Resume builder helps recruiters read, scan, and shortlist your Resume faster.

Use professional field-tested resume templates that follow the exact Resume rules employers look for.

Create Resume